Why Most Russians Will Stay Home for New Year’s

As Incomes Crumble, Even Celebrating with Friends Is Too Expensive for Them

Vladimir Ruvinsky

Vedomosti

December 27, 2018

New Year’s, apparently, has become a truly stay-at-home holiday. The number of Russians who plan to spend the long New Year’s holiday at home has jumped from 41% in late 2015 to 70% in late 2018, according to a survey by Romir, a Russian research company. The main reason is the rapid return to the conservative tradition of growing poverty and uncertainty in the future, combined with the desire to maintain previous levels of consumption of the most vital goods and services, which no longer include a winter holiday away from home.

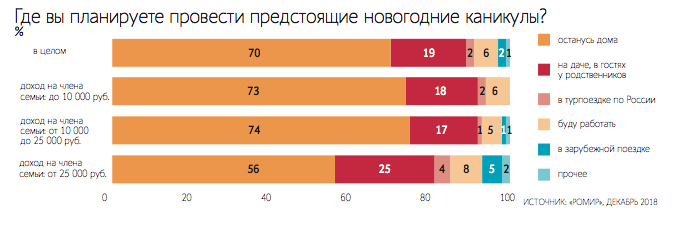

“How do you plan to spend the upcoming New Year’s holidays?” Overall: at home, 70%; at dacha, visiting relatives, 19%; traveling in Russia, 2%; working, 6%; traveling abroad, 2%; other, 1%. Average monthly income per family member of 10,000 rubles: at home, 73%; at dacha, visiting relatives, 18%; traveling in Russia, 2%; working, 6%. Average monthly income per family member of 10,000 rubles–25,000 rubles: at home, 74%; at dacha, visiting relatives, 17%; traveling in Russia, 1%; working, 5%; traveling abroad, 1%; other, 1%. Average monthly income per family member of 25,000 rubles or greater: at home, 56%; at dacha, visiting relatives, 25%; traveling in Russia, 4%; working, 8%; traveling abroad, 5%; other, 2%. Source: Romir, December 2018. Courtesy of Vedomosti

Surveys of the same representative selection of respondents have shown a drop-off in all other ways of spending the New Year’s holidays, which have basically become yet another period of time off work for Russians. The number of Russians planning to spend the holidays at the dacha or visiting friends or relatives has decreased from 34% to 19% in three years. Trips within Russia have dropped from 8% to 2%, while trips abroad have fallen from 4% to 2%. Nearly everyone has been scrimping, including Russians with above-median incomes. Fifty-six percent of Russian with monthly incomes of 25,000 rubles [approx. $364] per family memberwill stay home, as will 74% of Russians with monthly incomes between 10,000 rubles and 25,000 rubles per family member. As Tatyana Maleva, an economist from RANEPA, notes, the Russian urban middle class, which has grown accustomed to traveling, cannot afford it.

The picture emerging from the survey reflects the mood of many Russians. Since 2014, real incomes have fallen four years in a row, and all indications are they will be shown to have fallen in 2018 as well. According to Rosstat, the monthly modal income in in 2017 was 13,274 rubles [approx. $233], while the monthly median income was 23,500 rubles [approx. $412]. Given these circumstances, the ruble’s devaluation, which has made trips abroad more expensive, is not such an important factor. In December 2015, one dollar cost as much as it does currently, 67 rubles, and its value was rising.

Holidays at home are not cheap, either. In November 2018, the percentage of Russians who had noticed a rise in prices had grown in comparison with October 2018, according to the Russian Central Bank. Forty percent of Russians noticed upticks in prices for meat and poultry; 32%, rises in the price of petrol; 28%, rising prices for cheese and sausage; while 26% had noticed that milk and dairy products were more expensive. All of these goods are part of the home holiday menu.

In comparison with 2014, consumption levels have fallen. They have not returned to their previous levels. Attempting to wriggle their way out of poverty or maintain their previous income levels, Russians have taken out an ever-growing number of consumer loans, which have proven difficult to pay back. Every fourth Russian who had outstanding loans in 2015–2017 spent 30% of their incomes paying them off, note Olga Kuzina and Nikita Krupensky, economists at the Higher School of Economics, in an article entitled “The High Debt of Russians: Myth or Reality?” published in the November 2018 issue of the journal Voprosy ekonomiki.

Generally, the Russian populace has transitioned to a minimalist model of consumerism, notes Maleva. Scrimping begins literally with the New Year. As Romir’s survey indicates, this transition has become a trend that will, apparently, shape the strategies and tactics of Russian consumers in the future, too. The only thing that has not changed over the years is the president’s televised New Year’s greeting: it costs nothing.

Translated by the Russian Reader

The “handy lawyer” at a place calling itself the Civil Legal Defense Center promises to relieve people “of their debts 100% quickly and legally.” Photo taken in central Petersburg on 22 July 2018 by the Russian Reader

The “handy lawyer” at a place calling itself the Civil Legal Defense Center promises to relieve people “of their debts 100% quickly and legally.” Photo taken in central Petersburg on 22 July 2018 by the Russian Reader Reliable Future Consumer Credit Cooperative is one of many retail lenders ready to help ordinary Russians “boost their standard of living.” Photo by the Russian Reader

Reliable Future Consumer Credit Cooperative is one of many retail lenders ready to help ordinary Russians “boost their standard of living.” Photo by the Russian Reader