A year ago, Russian Central Bank chief Elvira Nabiullina triumphantly introduced the new Crimea-themed two hundred ruble banknote into circulation. Since the economy is shaped more by flows of goods, resources, people, services, knowledge, and money, and the actions of ordinary people, decision makers, and the snake oil salesmen known as capitalists, and less by puerile revanchist neo-imperalist symbolism, the new banknote, pegged at €2.90 by Deutsche Welle only a year ago, is now worth a mere €2.65. I am keeping my specimen as a souvenir of the current bad times until better days arrive. Image by the Russian Reader

A year ago, Russian Central Bank chief Elvira Nabiullina triumphantly introduced the new Crimea-themed two hundred ruble banknote into circulation. Since the economy is shaped more by flows of goods, resources, people, services, knowledge, and money, and the actions of ordinary people, decision makers, and the snake oil salesmen known as capitalists, and less by puerile revanchist neo-imperalist symbolism, the new banknote, pegged at €2.90 by Deutsche Welle only a year ago, is now worth a mere €2.65. I am keeping my specimen as a souvenir of the current bad times until better days arrive. Image by the Russian Reader

Fall in Real Incomes of Russians Accelerated Sharply in September

Economists Say Government’s Forecast No Longer Realistic

Tatyana Lomskaya

Vedomosti

October 17, 2018

Real incomes of Russians have declined for a second month in a row, Rosstat has reported. Their decline accelerated in September to 1.5% in annual terms after falling by 0.9% in August. Prior to that, they had grown for seven months, from the start of the year, by 1.7%. (This figure excludes the one-time 5,000-ruble payments made to pensioners in January 2017.) Real wages accelerated their growth in September, from 7.2% to 6.8% in the previous month.

Incomes of ordinary Russian had been falling for four years in a row, from 2014 to 2017, resuming growth only this year. In the first half of the year, they increased by 2.6%, mainly due to wage increases, notes Igor Polyakov from the Center for Macroeconomic Analysis and Short-Term Forecasting (TsMAKP). Business income increased only by 0.7%, while social transfers (excluding the one-time payment to pensioners) increased by 1.2%, which was significantly weaker than all incomes generally. Other sources of income decreased. There was a slight increase in incomes derived from property, but incomes received from securities and deposits decreased, as did, apparently, incomes from unreported activity, says Mr. Polyakov. He argues it is unlikely circumstances have changed considerably in recent months.

But the anxiety of Russians caused by the volatility of financial markets has increased, says Mr. Polyakov. People have taken to withdrawing cash from foreign currency accounts and transferring it to safe deposit boxes, as well as spending it abroad on holiday. Rosstat cannot register these expenditures and thus reduces its assessment of miscellaneous income. In August, the public’s net demand for US dollars grew by comparison with July from $0.8 billion to $1.7 billion, an increase of nearly 53%, the Central Bank reported.

Retail growth slowed in September to 2.2% in annual terms from 2.8% a month earlier. It is likely the public preferred buying foreign currency while curtailing consumption, argues Mr. Polyakov.

The drop in incomes combined with the serious increase in wages [sic] remains a mystery, writes Dmitry Polevoy, chief economist at the Russian Direct Investment Fund. The growth in real incomes in the first half of 2018 was mainly due to the presidential election campaign, notes Vladimir Tikhomirov, chief economist at BCS Global Markets. Salaries in the public sector and pensions increased rapidly. [That is, the Kremlin bribed Russians directly dependent on its largesse to get out the vote for President-for-Life Vladimir Putin—TRR.] After the election, growth stalled. And, after a palpable devaluation of the ruble in April and accelerating inflation, a dip in incomes was anticipated, argues Mr. Tikhomirov. In September, prices for imported goods rose. In addition, the seasonal discount on fruits and vegetables ended, and the July increase in utilities rates made itself felt, explains Mr. Tikhomirov.

By the end of the year, the incomes of Russians will gradually decline a little, while overall incomes will grow less than 1% on the year, predicts Mr. Tikhomirov. Real incomes might grow by 2% on the year, counters Mr. Polyakov. In any case, this is noticeably lower than official forecasts. The Russian Economic Development Ministry anticipated a 3.4% growth in real incomes in 2018.

Real incomes of ordinary Russians fell by 1.7% in 2017, although the government had forecast a 1.3% increase, the Federal Audit Chamber noted in its opinion on the draft federal budget for 2019–2021. When the forecast was corrected, incomes had decline dsteadily from the beginning of the year, and there were no preconditions for rapid growth by year’s end, the auditors write.

Income growth depends on whether private enterprise will increase wages, argues Mr. Polyakov, but thos wages will be subject to the planned rise in the VAT to 20% in 2019.

President Putin has set a goal of halving poverty by 2024. (The official poverty rate last year was 13.2% of the populace.) The Economic Development Ministry’s forecast significantly increased the growth rate of real wages and anticipated higher growth rates for real incomes, which has raised doubts at the Audit Chamber. There is no wage increase for public sector employees planned in 2019, while the growth of wages in the private sector will depend on growths in productivity.

Rank-and-file Russians have been forced into debt, write analysts from RANEPA and the Gaidar Institute in their opinion on the draft budget. By mid 2018, Russians owed banks 13.7 trillion rubles (approx. 181 billion euros), an increase of 19% from the previous year, they write, and an amount that significantly outpaces the increase in nominal incomes. It is an alarming trend that means an increase in the amounts of money ordinary Russians spend servicing loans, experts warn.

Translated by the Russian Reader

“3,500 rubles.” Graphic courtesy of Vedomosti. At the current exchange rate, 3,500 rubles is worth approximately 46 euros.

“3,500 rubles.” Graphic courtesy of Vedomosti. At the current exchange rate, 3,500 rubles is worth approximately 46 euros. The “handy lawyer” at a place calling itself the Civil Legal Defense Center promises to relieve people “of their debts 100% quickly and legally.” Photo taken in central Petersburg on 22 July 2018 by the Russian Reader

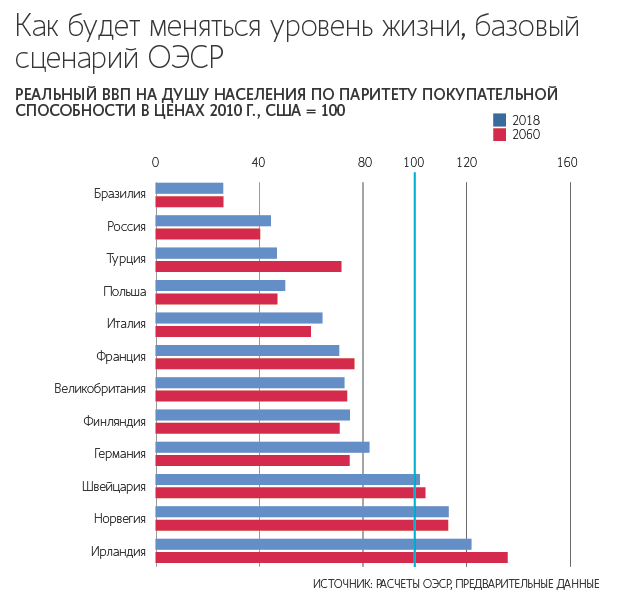

The “handy lawyer” at a place calling itself the Civil Legal Defense Center promises to relieve people “of their debts 100% quickly and legally.” Photo taken in central Petersburg on 22 July 2018 by the Russian Reader “Change Yourself for the Better.” If you read the following article, about the OECD’s forecast for economic growth in Russia, between the lines, you will discover a takeaway message that has been apparent to numerous observers for a long time. Until Russia does away with official kleptocracy, rampant corruption, outrageously bad governance, and the shock-and-awe policing of politics and business by the siloviki—i.e., unless it renounces Putinism and all its ways—there is little chance the living standards of ordinary Russians will improve much in the next forty years. Photo by the Russian Reader

“Change Yourself for the Better.” If you read the following article, about the OECD’s forecast for economic growth in Russia, between the lines, you will discover a takeaway message that has been apparent to numerous observers for a long time. Until Russia does away with official kleptocracy, rampant corruption, outrageously bad governance, and the shock-and-awe policing of politics and business by the siloviki—i.e., unless it renounces Putinism and all its ways—there is little chance the living standards of ordinary Russians will improve much in the next forty years. Photo by the Russian Reader

This one-ruble coin, minted in 2014 and sporting the newish symbol for the ruble, adopted in 2013, won’t buy you love or much anything else.

This one-ruble coin, minted in 2014 and sporting the newish symbol for the ruble, adopted in 2013, won’t buy you love or much anything else.